The Challenge of Managing Carbon Emissions in Saskatchewan’s Mining and Mineral Sector

The global consensus reached in the Paris Agreement is that governments and industry need to reduce the carbon footprint and “to accelerate and intensify the actions and investments necessary for a sustainable low carbon future.” According to the national climate action plan that Canada submitted in relation to the agreement, “Canada intends to achieve an economy-wide target to reduce its greenhouse gas emissions by 30% below 2005 levels by 2030.”

By Victoria Taras and Peter W.B. PhillipsThe global consensus reached in the Paris Agreement is that governments and industry need to reduce the carbon footprint and “to accelerate and intensify the actions and investments necessary for a sustainable low carbon future.” According to the national climate action plan that Canada submitted in relation to the agreement, “Canada intends to achieve an economy-wide target to reduce its greenhouse gas emissions by 30% below 2005 levels by 2030.”

Various countries are adopting distinct strategies to achieve their national goals, and Canadian provinces, which have different prospects from one another, have likewise signalled plans to pursue distinct strategies. The federal government must recognize provinces’ diverse needs and opportunities as it creates policies to honour its commitments under the Paris Agreement.

Recognizing Saskatchewan has unique challenges as a hub of uranium and potash production, a group of Saskatchewan’s experts gathered in early June 2016 to explore the issue. Operating under the Chatham House Rule, they included representatives from the Saskatchewan Ministries of the Economy and the Environment, Cameco, Potash Corp, the Saskatchewan Mining Association, and the International Minerals Innovation Institute, along with academics from economics and public policy. They examined Saskatchewan’s mining and minerals sector and carbon management challenges, and made a series of observations about policy choices available as input to federal government national carbon mitigation plan deliberations.

Economic Context

Canada's total greenhouse gas (GHG) emissions in 2014 were 732 megatonnes (Mt) of carbon dioxide equivalent (CO2 eq), about 20% above 1990 emissions. However, components of the total are important to note:

- GHG per unit of GDP decreased 32% from 1990 to 2014;

- GHGs emitted per person in Canada decreased by about 7%;

- In 2014, 264 Mt CO2 eq, or 36% of Canada's GHG emissions, came from 574 large facilities (i.e., operations that emit 50 Mt CO2 eq of GHGs or more per year); and,Canada's GHG emissions in 2013 accounted for less than 2% of global GHG emissions[i]; in 2012 Canada ranked 11th in terms of total emissions .[ii]

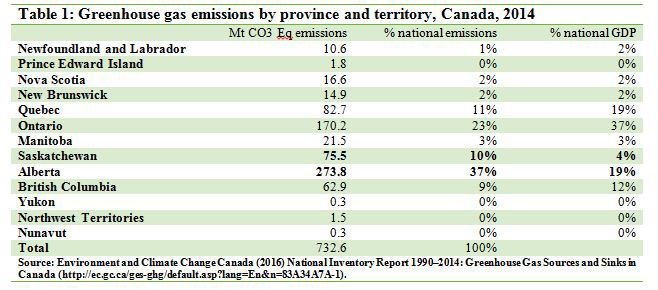

Distribution of emissions by province varies widely, partly based on the location of large facilities. Alberta and Saskatchewan each contribute proportionally more to national emissions than any other province; together, they contribute almost half the total, while accounting for less than one quarter of the national economy (Table 1).

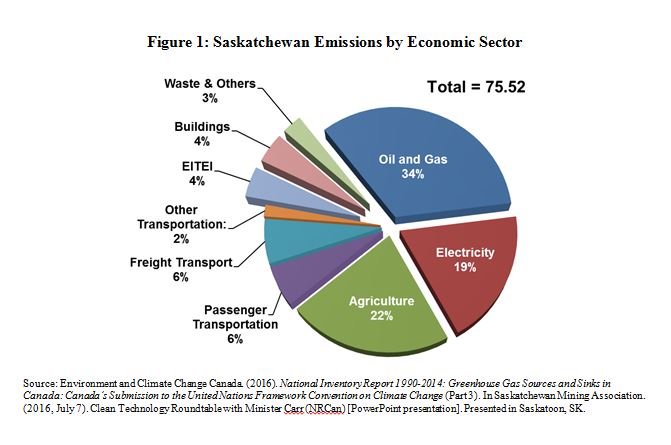

Saskatchewan’s contribution to GHG emissions is a function of its role as a major producer of energy products and as a consumer of significant energy to produce mineral, industrial, and food products. Potash and uranium, for example, are singular to Saskatchewan. The province has 42 large facilities emitting more than 50 kilotonnes CO2 eq of GHGs per year. A small proportion of that is emitted by the minerals and mining sector. The bulk of Saskatchewan emissions come from the oil and gas, agriculture, and electricity sectors, as shown in Figure 1, while the mining sector (which is part of the EITEI section in the figure) contributes slightly more than 3% of the total. Most of the products produced by large facilities in Saskatchewan are exported, but the province has limited market power, making it challenging to pass along incremental costs to consumers elsewhere.

The Policy Landscape

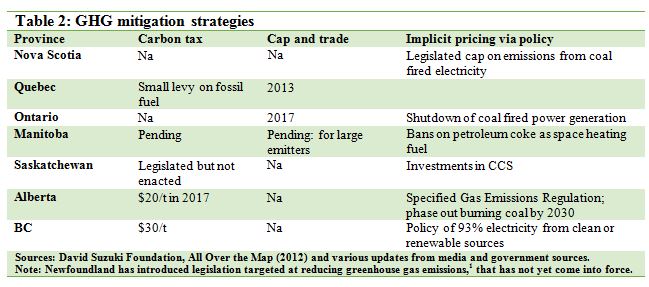

Many provinces have moved ahead of the federal government, implementing a mix of legislated direct pricing (via a carbon tax), cap-and-trade mechanisms (to generate a market price for carbon), and/or a mix of policy and investments to directly control or reduce carbon emissions. The Government of Saskatchewan has formed working groups to explore ways to reduce carbon emissions in the province. Regardless of approach, carbon is priced either by fiat, the market, or implicitly by the nature of the direct and indirect costs of specific mitigation strategies (Table 2).

Three broad types of carbon pricing options exist: carbon tax, carbon trade, and implicit carbon pricing.

Carbon tax is promoted as a way to plug a policy gap that might exist in certain jurisdictions, but it might not be the optimal strategy for Saskatchewan’s resource-based, export-dependent economy. While many assume that mineral products have market power allowing transfer of some tax to downstream markets and consumers, recent research suggests the high price elasticity of potash and uranium in both the short and long-term might compromise this transfer.[i] Many other Saskatchewan operators who sell in hotly contested global markets experience the same limitation. As a result, a tax would cause the net back to producers to drop, causing profits to fall and, all things being equal, a drop in production. This would have a number of effects, including:

- Reducing the tax base for Saskatchewan and Canada as profits and related employment income diminish;

- Encouraging companies to relocate production to operations in countries where carbon pricing is lower, but correspondingly, where the carbon emitted per unit of output may be higher; and/or

- Raising the carbon footprint of the sector globally while impeding efficient and profitable operation in Canada.

Furthermore, while the notion of a tax is both to encourage conservation and induce innovation, the first is ambiguous and the second is problematic in such a lumpy and capital intensive industry. It is often difficult and disproportionately costly to redesign or retrofit a plant in the minerals and mining sector to take advantage of new relative input prices.

Another popular strategy is cap and trade. It sets a limit on total carbon emissions, allocating rights to emit either by auction or by built capacity, then facilitating the transfer of these credits to be efficiently allocated between producers and consumers. Setting a cap below current emissions is intended to generate positive prices for the credits that can be efficiently (re)allocated through market trading to deliver the most efficient distribution of credits at the lowest aggregate cost.

While this resolves some of the inefficiencies of a flat tax on GHGs, it’s not perfect. New market entrants, which emerge often in mining, are disproportionately disadvantaged if they must purchase carbon allowances up front. They would thus be encouraged to seek a jurisdiction without cap and trade. In addition, logistical questions such as the best market size for the carbon trading (i.e., provincial, inter-provincial, or international) remain unanswered.

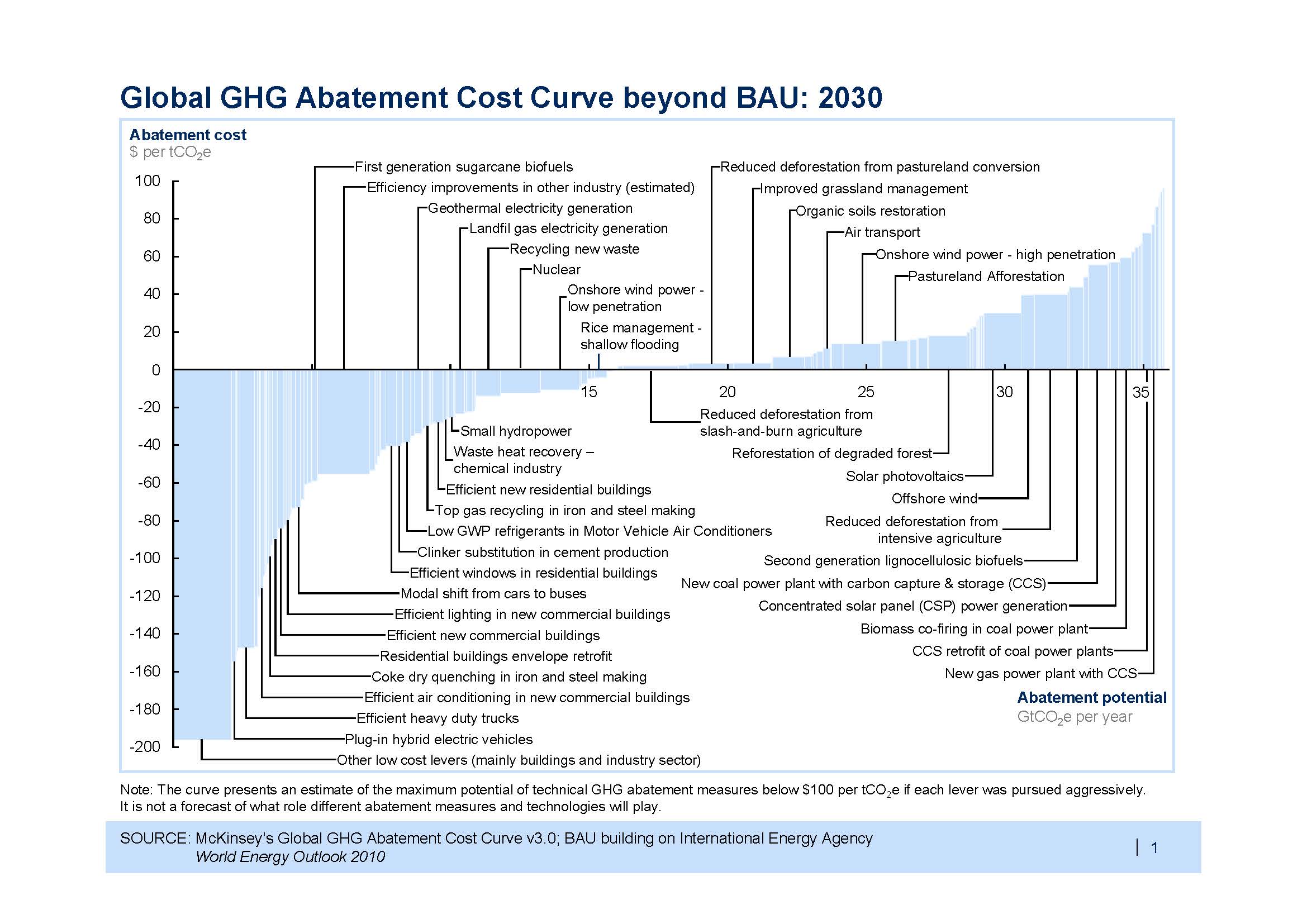

The final strategy is implicit carbon pricing, which occurs when governments either mandate the use of renewable energy sources or directly reducing carbon emission through investment. Both costs and benefits are internalized in specific policies and projects. Figure 2 shows one estimate of the net benefits or costs and the scale of carbon mitigated for a variety of policies, programs and investments. Companies’ marginal operating costs are increased by implicit costs.

Policy Considerations

Once a carbon pricing scheme has been determined, a carbon price must be set. The minimum price needed to meet carbon mitigation goals has been modelled several times over many years. The results have generally shown that the price would need to be very high in Canada to achieve the carbon mitigation targets.

Politically, a very high price is unacceptable. The price gets even higher if carbon pricing patterns are considered because carbon pricing policies tend to become more demanding with time regardless of the market. If the political climate allowed for high carbon prices, industry would be forced to implement severe changes that would likely adversely affect Saskatchewan activity, and/or companies would shift their mining activities internationally.

The mining and minerals sector’s uniquely cyclical nature can make it particularly difficult to determine an appropriate carbon price. If a company is able to survive a downcycle – as is currently the case – it might achieve success later during the upcycle phase. However, neither pure carbon tax nor pure carbon trade can capture nuances within the cycles.

For example, Europe has set its market price to follow the overall economic cycle,, but a company that is out of sync with the overall market risks overpaying during slumps and underpaying at peaks. Alternatives such as the auction process or the true-up process (i.e., closing off a carbon reduction commitment period) anchor the carbon price to what the rules and price may be in the future, which can lead to unforeseen consequences. In California there was a cessation of the purchase of new credits because new legislation was expected. Cyclicity must be accounted for when setting a carbon price, but doing it in a fair and sustainable way is tricky.

Neither carbon tax nor carbon trade functions accurately if carbon consumption cannot be measured. This is a problem of technology. There are mechanisms in place within Saskatchewan to measure the carbon consumption from most large-point sources, but not from gas wells where many emissions arise. No technology yet exists to accumulate the carbon from the gas wells to measure it, and only a tiny number of studies have been conducted to estimate the amount consumed. A similar situation exists in the agricultural industry, which is Saskatchewan’s second highest contributor of GHGs.

Technology and innovation inform other methods of carbon management. Clean energy, the ongoing ‘flavour of the year’, was emphasized in Canada’s national climate action plan that was submitted in relation to the Paris Agreement. Saskatchewan actively uses a range of technologies to reduce the province’s carbon footprint: the province has encouraged co-generation in one of its coal-fired power plants and in one potash mill, however past policy barriers prevented co-generation from being more fully utilised.

Possible technology innovation programs, where government funds research and development (R&D), have been examined through small laboratory studies in Alberta. According to the symposium attendees, such programs have a modest return because 80 per cent of R&D does not yield usable results. None of the studies has been translated into the field, and, if they were, governments would be unlikely to forgive their inherent costly and numerous failures. Insufficient support for technological innovation negates a host of other potential strategies such as cap and trade, which only works when appropriate technologies exist to allow offsets. Furthermore, if purchasing allowances is cheaper than purchasing the technology, then cap-and-trade risks being treated as a form of ‘indulgence’ where payment can negate ‘sins’, thus motivating companies to maintain high emissions when it is the cheaper option.

Other carbon management options exist. Importing energy into Saskatchewan, for example, could be done in small amounts, but is definitely not a big future strategic option. There is some potential to revise the royalty structures to encourage investments in GHG reducing technologies. Although they respond to changes in cost of mining and mineral products, royalty rates are already complex and don’t necessarily respond well to changes in underlying cost (e.g., if the cost of labour increases, ceteris paribus, the royalty levied for uranium is not likely to respond). This is less of an issue in the potash industry where operating costs are part of the royalty calculations. Meanwhile, carbon capture and storage (CSS) is being piloted in Saskatchewan, but it remains to be seen whether it will effectively and efficiently address the high GHG emissions in the sector.

Regardless of the carbon management option, Paris Agreement goals cannot be met unless targeting is extended beyond the big emitters to other supply-chain components. For example, the minerals and mining sector makes abundant use of materials that generate a large amount of carbon, such as cement. Moreover, most industrial operators draw significantly on the electricity grid, which, in Saskatchewan, is dependent on coal. Natural gas, which generates significant emissions as it is transmitted to the location where it will be distributed, is similarly used quite a lot within the province’s potash industry.

With so many variables at play, what should the federal government ultimately keep in mind when creating its carbon mitigation policy? Federal policies about carbon management must be mindful about the particularities of each province and their core industries. While any single order of government may be able to inform a simple and straightforward system, it seems likely that the cascading effect of federal, provincial, and interprovincial policies will create carbon pricing schemes that employ a multiplicity of mechanisms (i.e., tax, trade, and implicit pricing), none of which work well in isolation. An excessively high or rigid carbon price, in addition to the implicit price of direct policy interventions, could incentivize companies to make dramatic changes that can be detrimental to employment in provinces that depend on industries with high levels of carbon emission, and, by the nature of their supply chains, in other provinces.

Four key considerations have been identified:

- switching to renewable energy often results in implicit costs borne by the mining and minerals sector;

- policy must be responsive to the cyclicity of the industry, which is often too volatile for timely government reaction;

- layering of carbon pricing by pursing taxes, trading, and implicit pricing compounds challenges for many operators; and,

- industry has special insights that should be drawn into the policy discussion.

Ultimately, any harm done at the provincial level undercuts federal objectives of generating a sustainable and prosperous economy and society. Policymakers should be especially mindful of the inherent cyclicality and capital-intensive nature of the Canada’s resource sector—additional time may be required by the industry to respond to new policies, and once investment decisions are made they tend to be long-lived.

Conclusions

References

- http://unfccc.int/paris_agreement/items/9485.php

- http://www.climatechange.gc.ca/default.asp?lang=En&n=E18C8F2D-0

- National Resources Canada. (2015). Energy Fact Book 2015-2016, p. 100. https://www.nrcan.gc.ca/sites/www.nrcan.gc.ca/files/energy/files/pdf/EnergyFactBook2015-Eng_Web.pdf

- https://www.ec.gc.ca/indicateurs-indicators/default.asp?lang=En&n=FBF8455E-1

- Quddus, M. Abdul, Siddiqi M. Wasif, and Riaz Malik M. “The Demand for Nitrogen, Phosphorus and Potash Fertilizer Nutrients in Pakistan.” Pakistan Economic and Social Review 46, no. 2 (2008): 101-16. http://www.jstor.org/stable/25825330.

Victoria Taras

Victoria Taras is a PhD student at the Johnson Shoyama Graduate School of Public Policy at the University of Saskatchewan. She primarily researches disability policy implementation under the guide of supervisor Dr. Brett Fairbairn. She also researches co-operatives with Dr. Lou Hammond-Ketilson and organ transplant ethics with Dr. Amy Zarzeczny as part of the CHIR Canadian National Transplant Research Program.

Peter W.B. Phillips

Peter Phillips is a distinguished professor at the Johnson Shoyama Graduate School of Public Policy. He holds a PhD in International Political Economy from the London School of Economics, and has practiced for 13 years as a professional economist and senior policy advisor in Canadian industry and government.